Your Vendor Is Your Competitor

Why the frontier labs are aggressively adding services arms and what that means

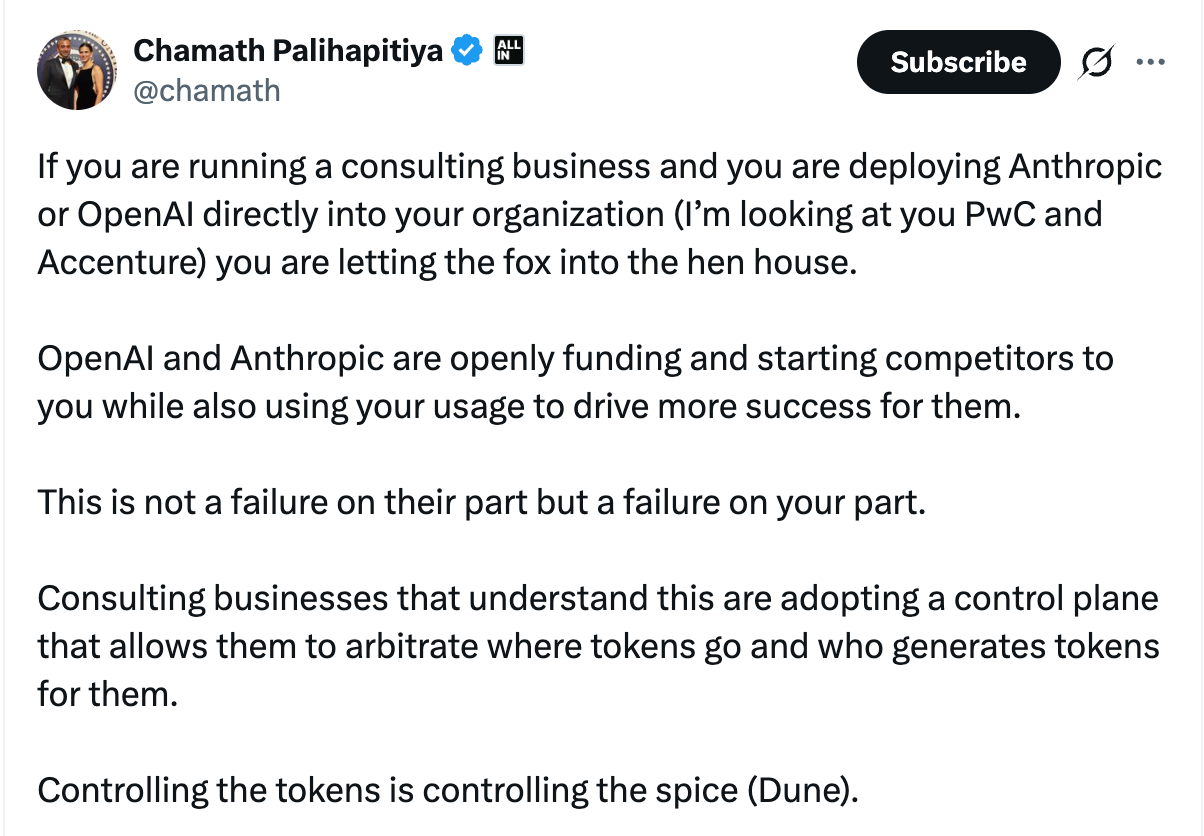

Any listener of the All In podcast knows Chamath is full of hot takes, for better or for worse.

A few weeks ago he did make a very salient point: consulting businesses running Anthropic and OpenAI are “letting the fox into the henhouse”.

So what prompted this take?

On May 4th, Anthropic announced a $1.5 billion joint venture with Blackstone, Hellman & Friedman, and Goldman Sachs — backed by Apollo, General Atlantic, GIC, Leonard Green, and Sequoia — to embed engineers directly inside mid-sized companies and deploy Claude into core business operations.

A week later, OpenAI launched the “OpenAI Deployment Company” with $4 billion in funding at a $14 billion valuation, backed by TPG, Bain Capital, Brookfield, and — amazingly — McKinsey, Bain & Co., and Capgemini as equity investors. OpenAI simultaneously acquired Tomoro, an applied AI consulting firm, bringing 150 forward-deployed engineers on day one. Oh, and Goldman backs both ventures. And just a few weeks before all of this, Google Cloud committed $750 million to fund consulting partners including Accenture, Deloitte, and McKinsey for agentic AI deployment.

So in the span of a few weeks, the three most important AI platforms on the planet made major moves into the services and consulting realm. They didn’t tiptoe into it. They showed up with billions of dollars, acquired a consulting firm, and partnered with PE firms that collectively sit on the boards of thousands of mid-market and enterprise businesses.

Our view: if you’re a startup building on foundation models, or a consulting firm advising clients on AI adoption, this is the most consequential development of the year — and be aware that your vendor may become your number one competitor.

The Palantir Playbook

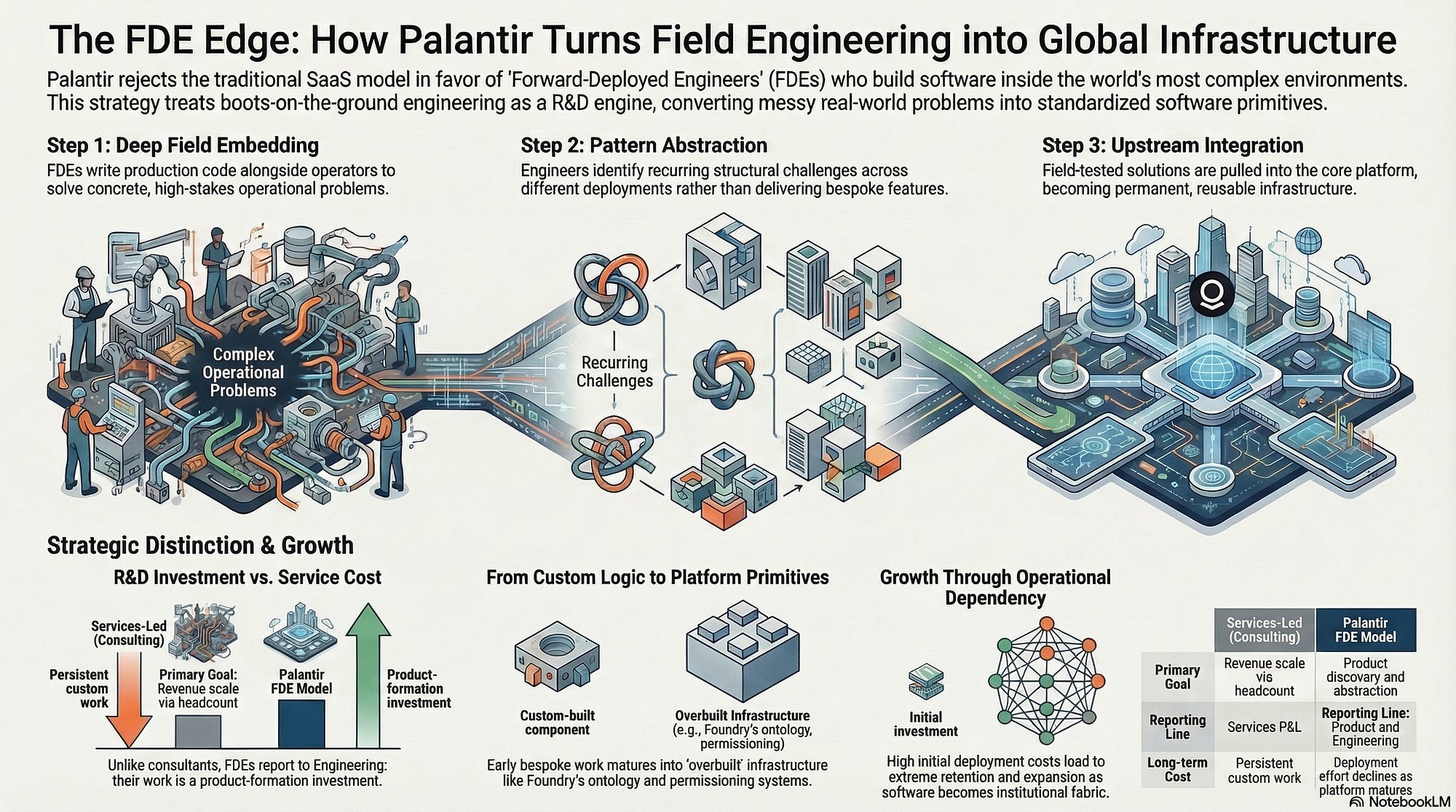

This isn’t a random pivot into services. Both OpenAI and Anthropic are explicitly copying the model that turned Palantir from a perpetual “when will they figure it out” story into a $250B+ juggernaut — the forward-deployed engineer.

FDEs don’t install software. They embed inside client organizations, sit with your teams, map your messy data environments, redesign your workflows, and build production systems that tie into the reality of how you actually operate. Palantir’s insight was that these engineers weren’t a cost center or a professional services drag — they were the company’s primary product discovery engine. Every ugly integration, every weird edge case, every workaround they encountered in the field got fed back and abstracted into platform capabilities that made the next deployment faster and cheaper. That flywheel is what drove Palantir’s U.S. commercial revenue up 137% year-over-year and produced a 640% stock return over five years.

But here’s what makes the AI labs’ version of this potentially more dangerous for the ecosystem: Palantir was deploying its own proprietary platform. OpenAI and Anthropic are deploying the same models that thousands of startups build on top of. When DeployCo’s FDE walks into a Fortune 500 account and builds a custom AI system using GPT, that company is much less likely to also buy your startup’s vertical wrapper. The platform vendor now owns the model, the implementation, the customer relationship, and the feedback loop. That’s a level of vertical integration Palantir never achieved.

This is fundamentally the AWS playbook repeating. Amazon spent years building a cloud platform, let thousands of startups flourish on it, then systematically built its own versions of the most popular services. The thin-wrapper startups died first. The ones with real differentiation survived — but they had to be brutally honest about where their moat actually was. The difference this time is the speed. AWS took a decade to move meaningfully into services. OpenAI went from “API company” to “$14 billion consulting arm” in under three years.

Who Gets Squeezed

Three groups are in the crosshairs.

AI startups building on foundation models. The existential risk is pretty straightforward. If DeployCo is sending 150+ engineers into enterprise accounts to build custom deployments using OpenAI’s own models, what happens to the startup that was selling a vertical AI product built on the same API? The startup’s pitch was “we understand your industry better than the lab does.” The lab’s counterpitch is now “we’ll send engineers who understand the model better than anyone, backed by $4 billion and TPG’s portfolio of 2,000+ companies opening doors for us.”

Consulting firms. Axios had the best line on DeployCo’s launch: OpenAI “somehow convinced these legacy firms to help fund their own disintermediation.” McKinsey and Bain & Co. are equity investors in a company that exists to do, with forward-deployed engineers and the world’s best language models, a version of what those firms charge $500/hour junior associates to do. The generous read is they’re buying a seat at the table — early model access, a role in the deployment ecosystem. The less generous read is they’re funding a front-row seat to their own disruption. Fortune’s coverage of the Anthropic venture framed it cleanly: for every dollar companies spend on software, they spend six on services. That 6:1 ratio is what built consulting into a multitrillion-dollar industry. And it’s what makes the consulting market the juiciest target for AI labs that need to show revenue growth ahead of their IPOs.

Enterprise buyers (the hidden risk). CIOs are being offered something seductive: the model provider’s own engineers, embedded in your organization, building your AI systems. But as one CIO analyst put it, these FDEs “see the formal architecture and the informal workaround. They see the process map and the exception queue. They see what the enterprise says it does and what it actually does on a difficult Tuesday afternoon.” If OpenAI retains majority control of DeployCo, and DeployCo’s engineers are inside your systems, who governs the data boundary? Who owns the operational knowledge they accumulate? These are real questions that most buyers aren’t asking yet.

Owning Your Destiny

So what does this mean if you’re building or investing in AI?

It forces a level of honesty that a lot of startups have been avoiding. Here’s where we think defensibility actually lives in a world where the model vendor has an FDE in your customer’s office:

Proprietary data and domain expertise that the labs can’t replicate in a six-week engagement. If your company has accumulated years of domain-specific data through thousands of customer interactions — real contract negotiations, real threat intelligence, real clinical decisions — that’s something a generalist FDE simply cannot walk in and reproduce. The companies we invest in that look most durable right now are the ones where the product gets better with every customer deployment, and that accumulated advantage is nearly impossible to fast-follow.

Multi-model architecture as an existential imperative, not a technical preference. If your product only runs on one lab’s models, you’ve built your house on your competitor’s land. The labs have made this explicit — their services arms exist to drive adoption of their models specifically. Anthropic’s venture exists to “rapidly bring Claude into core business operations.” DeployCo exists to deploy “OpenAI’s models.” Startups that run on multiple models and make switching easy can credibly tell enterprise buyers: “We work for you, not for the lab.” That’s a differentiated position when the alternative is an FDE whose employer is the model vendor.

Going deep rather than wide. The FDE model is expensive. These ventures will inevitably prioritize the largest, most lucrative accounts — the ones backed by their PE partners’ portfolios. The opportunity for startups is in the long tail: industries too niche, companies too small, workflows too specialized for a generalist FDE to learn in six weeks. Deep vertical expertise and purpose-built products for underserved segments are harder to commoditize than horizontal “AI for everything” plays.

Owning the customer relationship upstream. If the lab’s FDE is the first technical person in the room, the startup has already lost. The companies that survive platform-vendor competition are the ones that own the customer relationship before the vendor shows up — through community, content, trust, and domain credibility. This is why companies with deep practitioner communities and years of embedded customer trust have structural advantages that no FDE deployment can easily replicate.

What Are You Building For?

There’s a question we often ask founders now that we never asked before: what happens when your model provider sends an FDE into your biggest customer? If the answer is a blank stare or something about relationships and trust, that’s not ideal. The companies that can answer it clearly — because they own proprietary data, because they’ve built on multiple models, because the customer is locked in through workflow and domain expertise rather than a monthly invoice — those are the ones worth backing.

Anyone who lived through AWS already knows the script. The platform lets you build, watches where the money goes, then shows up with more capital and better distribution than you have. The labs just did it faster and less subtly than Amazon ever did — going from API company to billion-dollar consulting arms in under three years, with PE firms opening the doors to thousands of enterprise accounts on day one.

For startups this doesn’t mean it’s over. But the margin for wishful thinking is gone. The ones that survive will have built something the FDE can’t replicate in a six-week engagement — real proprietary data, real domain depth, real customer trust. Not a wrapper, and not an assumption that the model vendor would stay in the model business.

The platform always comes for you. The question is whether you saw it coming.